Local currency shift

The majority of foreign inflows into emerging market fixed income assets over the past couple of years have gone into hard currency debt making the asset class “less attractive from a valuation perspective on a longer-term basis,” Spillane says. “As a result, we expect flows to become more balanced towards local currency,” he says.

The surge in emerging market debt issuance over the past few years has seen governments try to tap domestic capital markets by issuing bonds in local currencies.

This shift has a number of implications. A domestic buyer base means that these markets are less vulnerable to the vagaries of global capital flows.

“Fixed income markets in Colombia, Peru and Chile, for example, are being buttressed by strong demand from local pension funds that must hold domestic debt for regulatory reasons.

Local investors are also boosting liquidity in Russia, the Middle East and East Asia,” says Spillane.

“We still expect fairly attractive risk-adjusted returns in hard currency debt but nowhere near as strong as the valuation dynamics we expect in local currency.”

“Emerging market yield curves are very attractive across a number of markets such as Brazil, Colombia and Chile, which have offered a spread premium of close to, or above, 150bp,” says McDonagh.

Tapering threat

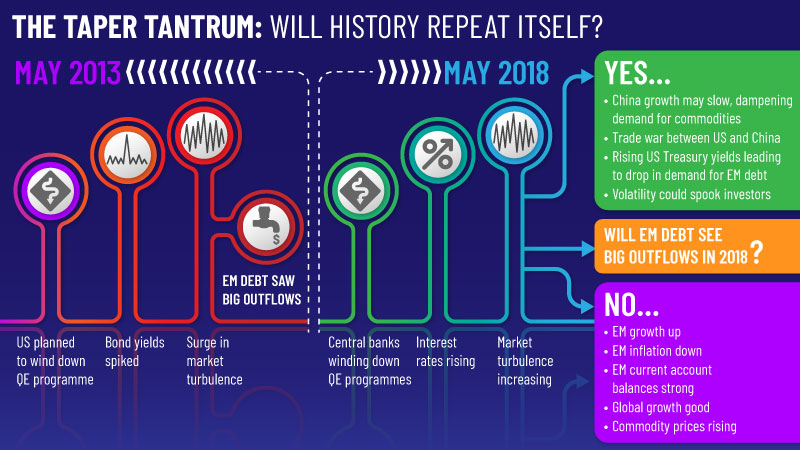

It remains to be seen how emerging market securities react to a sudden rise in US Treasury yields. Almost a decade of low interest rates in the developed world has encouraged investors to seek yield in emerging economies, but this era is coming to a close.

The European Central Bank and the Bank of Japan have followed the Fed in winding down their asset-buying programmes – monetary tightening will inevitably follow.

“It’s going to get choppier,” says Yerlan Syzdykov, deputy head of emerging markets at Amundi.

“Now tapering starts in earnest, funding will be squeezed and interest rates will rise in the developed world, which may put pressure on emerging markets. If there is significant volatility, the positive flows we have seen into local currencies may change quickly. We all have memories of the taper tantrum in 2013. It could replay again,” Syzdykov says.

“We do not expect it will be a disastrous year for emerging markets where investors take their money and run, but the rebalancing process could cause underperformance and pressure on the flows side.”

A sudden reversal of flows from emerging markets-focused exchange traded funds – which have multiplied since the taper tantrum – could fuel higher volatility.

Another possible spanner in the works is China. Growth in the world’s second-largest economy is widely expected to slow this year as Beijing cracks down on rampant public debt and imposes curbs on factory pollution.

“The elephant in the room with regards to emerging markets is always China,” says Lefteris Farmakis, global macro strategist at UBS. A Chinese slowdown could dampen demand for commodities, which would have a knock-on impact on the emerging world.

The impact of a possible trade war between China and the US is another concern and there is the ever-present spectre of political risk. Left-wing populist candidates could prevail in presidential elections in Brazil, Columbia and Mexico – three of Latin America’s largest economies – which might undermine investor confidence.

Spillane, however, remains positive. “There will be winners and losers across the emerging world as we move into a period of higher rates and more volatility but we are not expecting significant underperformance. We expect investor appetite to remain strong.”